Measuring Market Asymmetry: The Glassnode Skew Index

We've constructed a comprehensive measure of how options markets price asymmetric risk.

When assessing options markets, one of the most powerful signals is skew: how the market prices risk on the upside versus the downside. The standard approach for traders is to look at the 25-delta skew: a simple comparison between the implied volatility of a 25-delta call and a 25-delta put. This method is effective, simple and familiar, but it samples only two points on the volatility curve. As a result, it often misses structure embedded in the rest of the surface.

The Glassnode Skew Index addresses this by aggregating information across the full smile, producing a more robust signal of where risk is being priced. We explain the purpose of the new metric, how it is constructed, and how it can fit into the broader toolkit of options analysis.

To access the new metrics visit Glassnode Studio . Available to Professional plan users.

Introducing the Glassnode Skew Index

Instead of focusing on two isolated strikes, the Glassnode Skew Index condenses the entire shape of the volatility smile into a single, intuitive measure of market asymmetry.

We divide the curve into two regions: one representing downside risk, and one representing upside potential. Each region is transformed into a standardized volatility measure as we calculate how much volatility the market is pricing into that segment.

- DownVol represents the total implied volatility from out-of-the-money put options — protection against falling prices. When traders rush to buy puts, DownVol rises, signalling fear or a desire to hedge.

- UpVol captures the opposite: the total volatility priced into out-of-the-money call options. This reflects how much traders are willing to pay for upside exposure or potential short-squeeze gains. When call demand increases, UpVol rises, often alongside strong bullish sentiment.

The difference between these two components gives us the skew index: Glassnode Skew Index = UpVol - DownVol

- Positive values indicate a market that’s paying more for upside volatility – typically driven by optimism, momentum, or speculative call buying.

- Negative values mean downside protection dominates, as investors prioritize safety and hedging over chasing upside.

In practical terms, The Glassnode Skew Index shows whether option traders are more concerned about a crash down, or more excited about a breakout up – and by how much.

View live Chart

View live Chart

View live Chart

View live Chart

How to Use the Skew Index

The Skew Index can be applied in several ways to interpret options market positioning, identify sentiment regimes, and understand how traders are distributing risk across upside and downside scenarios.

Map the Current Sentiment Regime

The index can help contextualize prevailing market conditions:

- Deeply negative values indicate a market that is paying a premium for downside protection, consistent with defensive positioning.

- Strongly positive values indicate that investors are paying more for upside participation, often in the context of strong trends and speculative call activity.

Monitoring these extremes helps identify when fear or euphoria dominates the options market.

Use it as a Confirmation or Divergence Tool

The index can complement movements in spot price:

- A rising Skew Index alongside a rising spot price suggests that the options market is reinforcing the move through increased demand for upside volatility.

- A rally in spot with a Skew Index that stays sharply negative points to a distrusted move, where traders remain hedged and cautious.

- A falling market with a heavily negative Skew Index confirms a classic risk-off environment with significant demand for protection.

- A falling market with a positive Skew Index can indicate that traders are already looking through the weakness and positioning for a recovery.

This makes the index useful for evaluating whether options flows validate or contradict price action.

Interpreting Tenor Combinations

Different tenors can convey different layers of sentiment:

- A negative 1-week skew with neutral or positive 3- and 6-month values often indicates temporary stress overlaying a constructive medium- and long-term outlook.

- A very positive 1-week skew with subdued longer tenors suggests that traders are enthusiastic about the near-term, but reluctant to extend risk far into the future.

- When skew is consistently elevated or depressed across all tenors, it points to a stable, regime-like sentiment environment rather than a short-lived spike.

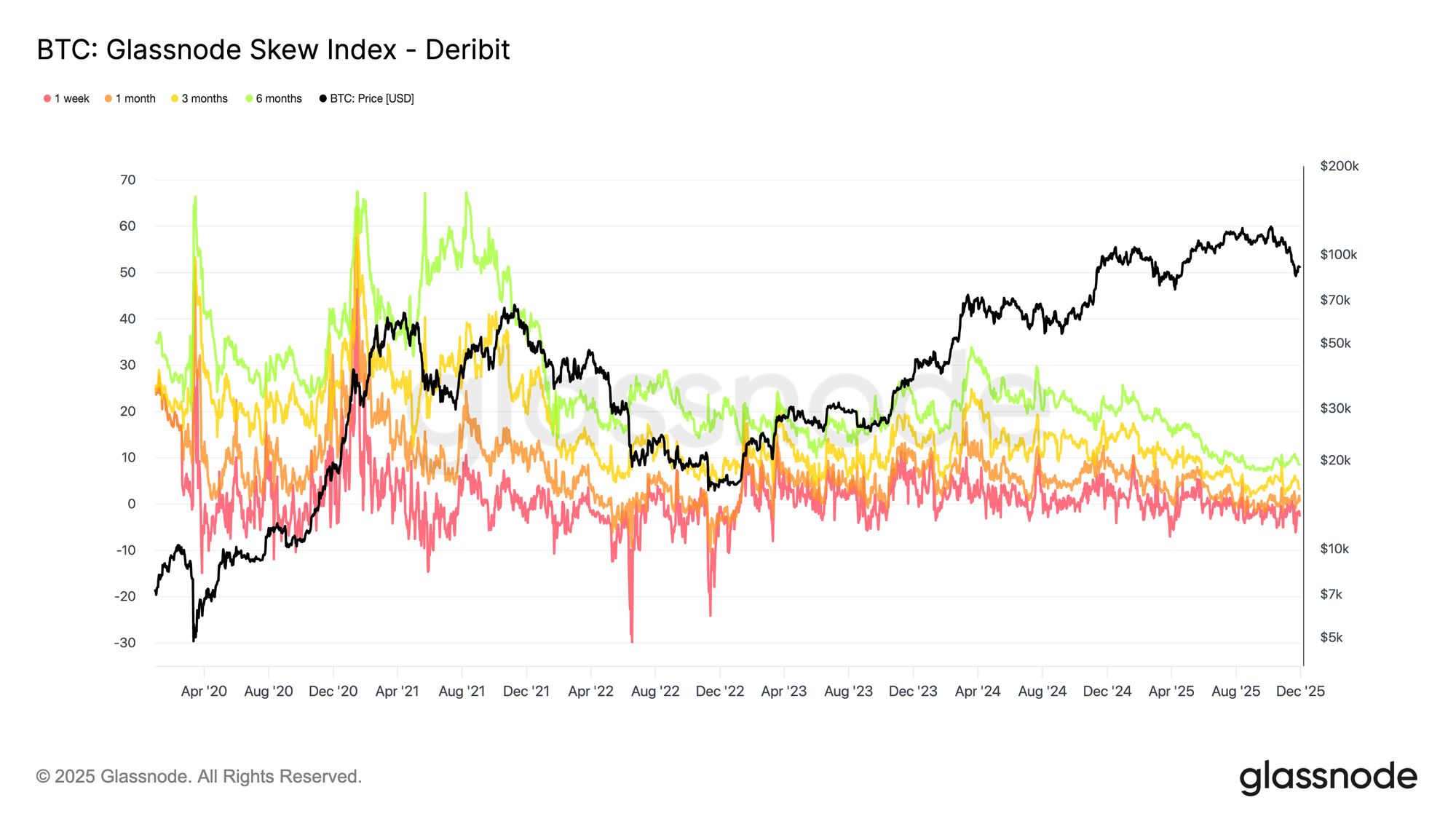

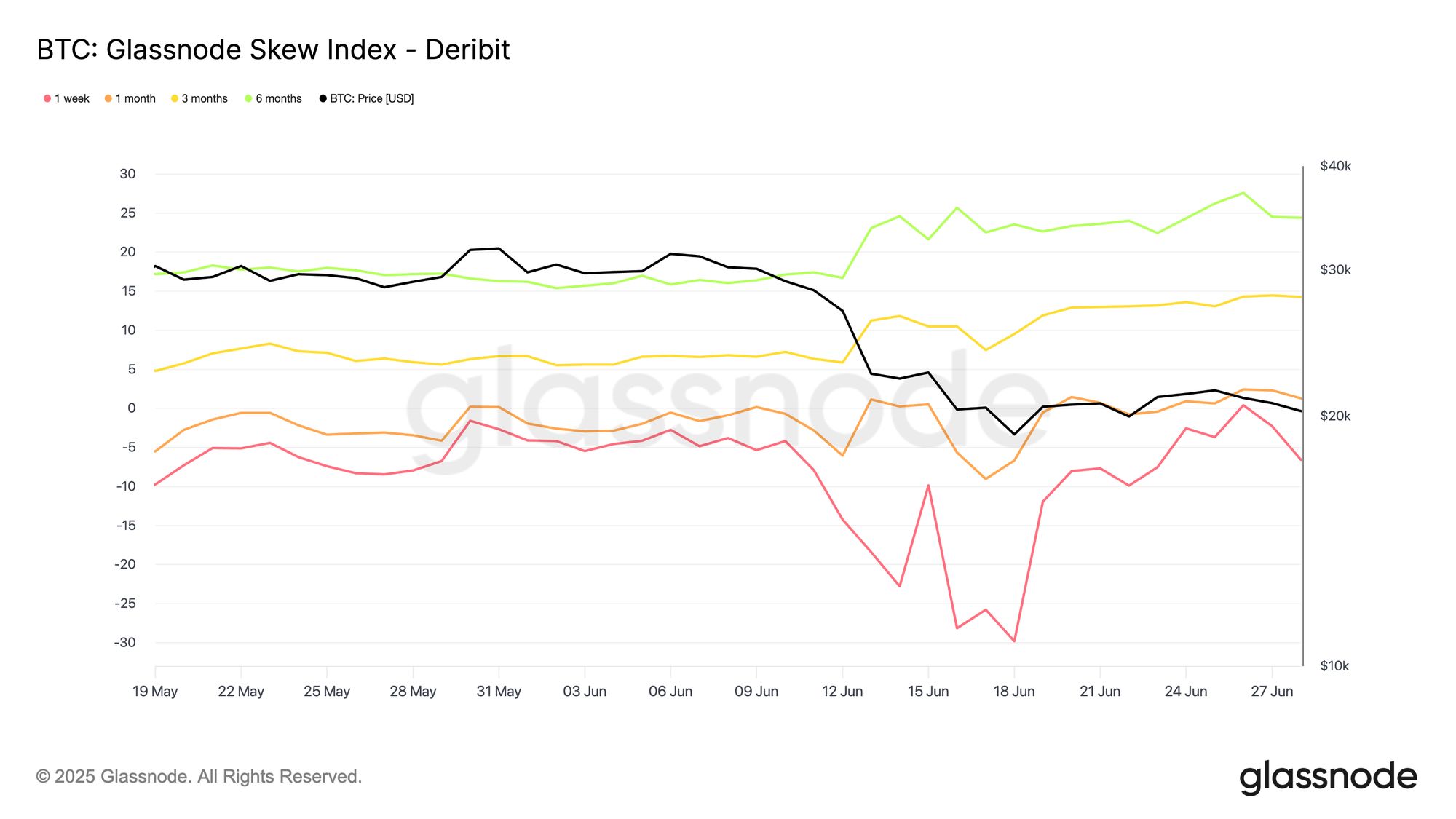

For example, in June 2022, we saw a clear tenor divergence: the 1-week Skew Index (red) plunged into deeply negative territory, signalling aggressive demand for short-dated puts over calls. Meanwhile, the 3-month (yellow) and 6-month (green) skews moved higher, indicating that investors were still willing to pay relatively more for upside exposure further out the curve.

In other words, the fear was mainly short-term, and longer-dated options continued to lean towards upside scenarios, implying that many participants expect better prices further out on the horizon.

View live Chart

View live Chart

How it Works Under the Hood

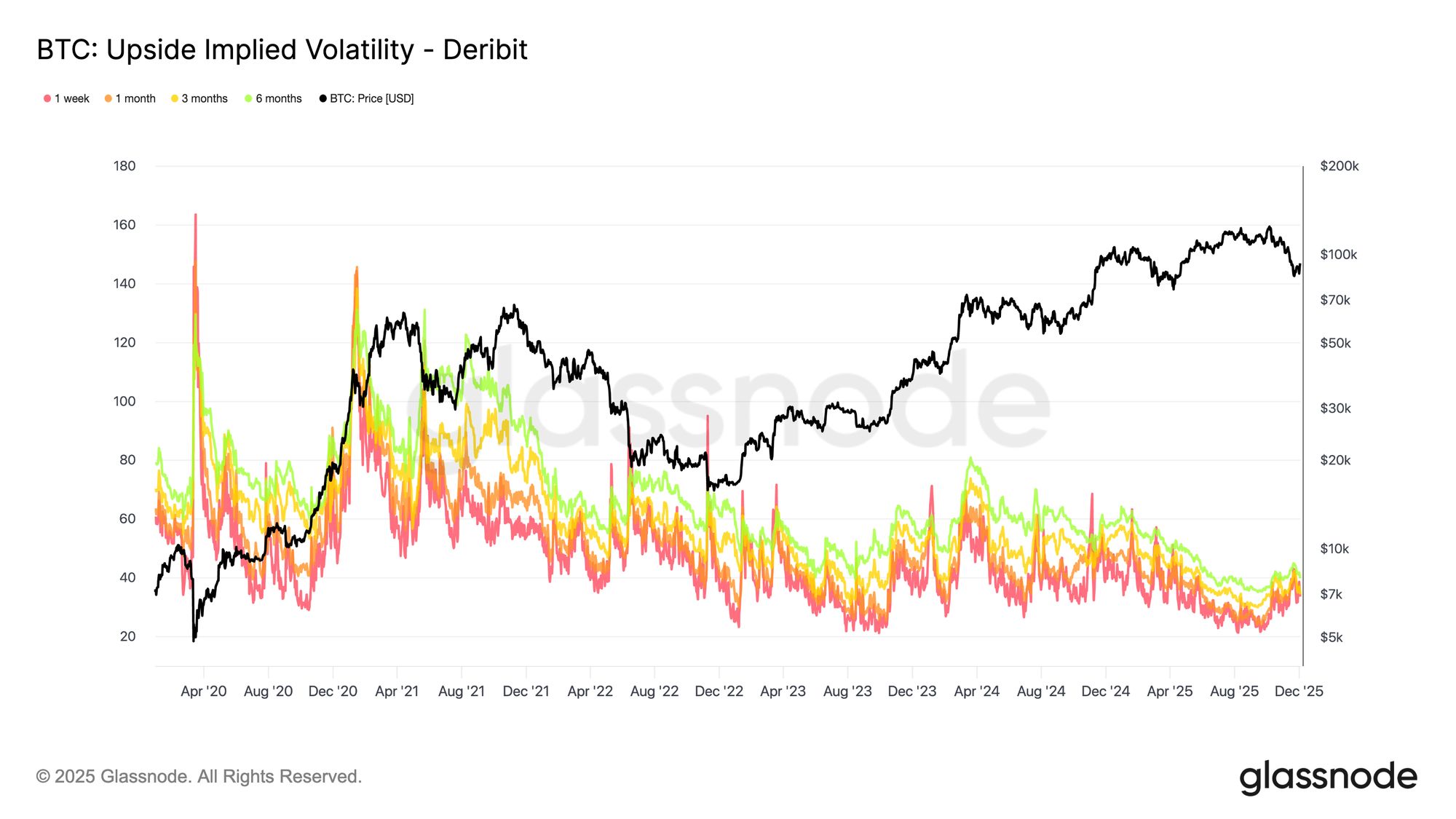

We calculate the Glassnode Skew Index by aggregating option prices across many strikes on both sides of the distribution. These prices are transformed into standardized measures of upside and downside implied volatility, aligned to fixed maturities such as 1 week, 1 month, 3 months, and 6 months.

We then combine data across major venues so traders can compare BTC, ETH, SOL, XRP, or PAXG on consistent terms. This standardization removes the distortions that arise from strike irregularities, liquidity gaps, or exchange-specific conventions.

The result is a cross-asset, cross-tenor gauge of options market sentiment that captures the full structure of the volatility smile rather than relying on a single-point skew measure.

Available for:

- Resolutions: 10 minutes, hourly, daily

- Tenors: 1 week, 1 month, 3 months, 6 months

- Assets: BTC, ETH, SOL, XRP, PAXG

- Exchanges: Deribit, OKX

Options data is a major focus for Glassnode's product development. We are scaling our coverage with new metrics that extend the depth of our volatility tooling, broaden analytical use cases, and give professionals a more complete view of positioning and risk across the market.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

The Emergence of CFTC-Regulated Clean Energy Platforms and Their Influence on Institutional Investment Approaches

- CFTC-approved CleanTrade, the first SEF for VPPAs/RECs, transforms clean energy markets by addressing liquidity, transparency, and regulatory challenges. - Its $16B trading volume and Cargill-Mercuria's first transaction demonstrate institutional adoption of standardized, verifiable renewable energy assets. - CleanTrade enables ESG alignment through project-specific carbon tracking, reducing emissions by 15% for investors while complying with IRA-driven $2.2T global investments. - By bridging financial a

Clean Energy Market Fluidity and the Rise of CleanTrade: Strategic Considerations for Investors in a Regulatory Environment

- CleanTrade, a CFTC-approved SEF, addresses fragmented pricing and low liquidity in clean energy markets by standardizing VPPA, PPA, and REC trading. - The platform’s $16B in two-month transactions demonstrates institutional demand for transparent, ESG-aligned tools to hedge energy risks and track carbon impact. - By centralizing renewable derivatives and aligning with regulations like SFDR, CleanTrade lowers barriers for investors and developers, accelerating decarbonization while boosting market efficie

The Rise of a Dynamic Clean Energy Marketplace

- Global clean energy investment hit $2.1 trillion in 2024, driven by decarbonization trends and institutional demand. - REsurety's CFTC-approved CleanTrade platform addresses liquidity gaps by standardizing VPPA/REC trading with oil-like transparency. - The platform processed $16 billion in two months, enabling risk mitigation and rapid capital reallocation amid policy shifts. - Advanced analytics and structured workflows transform clean energy assets into tradable instruments, attracting diversified inst

The Rise of a Dynamic Clean Energy Market and What It Means for Institutional Investors

- A liquid clean energy marketplace is emerging, enabling institutional investors to trade renewable assets with traditional market efficiency. - E-fuels and platforms like CleanTrade ($16B in notional value) address hard-to-decarbonize sectors while Enel's blockchain-based systems enhance scalability. - Regulatory reforms (e.g., EPA RFS) and industry M&A activity support market growth, though high costs and fragmented standards remain challenges. - 84% of institutional investors plan to increase clean ene