The Bitcoin Retirement Era

A new era of cryptocurrency retirement investment has begun.

A new era of crypto retirement investing has begun.

Written by: Thejaswini M A

Translated by: Block unicorn

For most of the 20th century, the answer to this question was simple: your employer decided. Companies provided pensions, managed investments, and bore the risk. If the fund performed well, they kept the extra gains; if it performed poorly, they made up the shortfall. You had no say, but you also bore no losses.

Subsequently, the advent of the 401(k) plan shifted responsibility to individuals. You choose the investments and bear the risk. But your choices are not entirely free. Employers still act as gatekeepers, offering only a set of "prudent" options. Initially, courts considered ordinary stocks too risky for retirement accounts. Later, index funds were seen as too passive. The definition of prudence has evolved, but the paternalistic approach remains.

On October 15, 2025, Morgan Stanley redrew the boundaries. The company’s 16,000 financial advisors can now recommend bitcoin investments to any client, including those with IRAs and 401(k)s. There are no minimum wealth requirements and no aggressive risk tolerance requirements. Bitcoin now quietly sits alongside bonds and blue-chip stocks in portfolios funding American retirement.

The risks are enormous. Total U.S. retirement assets amount to $45.8 trillions. Even if only 1% of assets are allocated to crypto, that means $270 billions flowing into the market. If it’s 2%, that’s over $500 billions.

What is the beautiful mathematical principle behind this? I have some thoughts to share.

Morgan Stanley Ushers in a New Era of Crypto Retirement Investing

Until October last year, Morgan Stanley restricted crypto access to clients with over $1.5 millions in assets, aggressive risk tolerance, and taxable brokerage accounts. Retirement accounts were completely prohibited.

Now, these restrictions are gone.

Advisors do not directly purchase bitcoin for clients. Instead, they allocate funds to regulated crypto investment products, primarily bitcoin ETFs from BlackRock and Fidelity. In the future, once approved, this may include Ethereum and Solana ETFs.

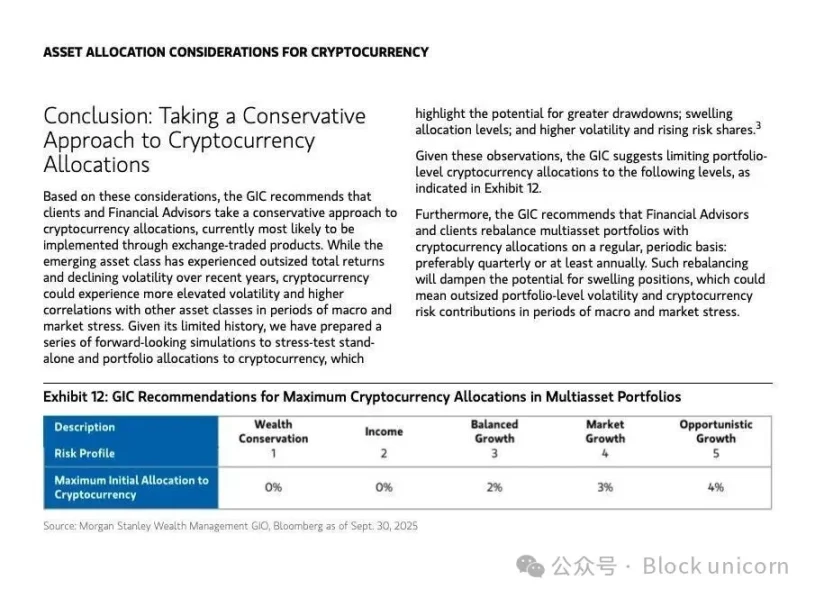

The company’s automated portfolio system tracks each client’s crypto exposure in real time to prevent over-concentration. Morgan Stanley’s Global Investment Committee recommends a 4% allocation for “opportunity growth” portfolios for young or aggressive investors, 2% for balanced growth portfolios, and 0% for preservation or income strategies.

These restrictions serve as legal shields. Under the Employee Retirement Income Security Act (ERISA) of 1974, which governs retirement plans and defines “prudent” investing, companies sponsoring 401(k) plans have a fiduciary duty to act in participants’ best interests. If a company offers imprudent or overly risky investments without proper oversight, participants can sue for losses. To win, plaintiffs must prove the trustee breached their duty by offering unsuitable investments or insufficient monitoring.

Morgan Stanley’s 4% cap and real-time risk monitoring are designed to defend against such lawsuits. The company is betting that conservative allocation limits and real-time risk monitoring will protect it from accusations of negligently exposing retirees to crypto volatility. Whether this defense holds when bitcoin drops 70% remains untested.

Advisors must record crypto recommendations through internal systems. Compliance teams ensure clients acknowledge volatility disclaimers and risk tolerance adjustments before investing.

While bitcoin ETFs are immediately available, Morgan Stanley’s E-Trade platform will launch direct trading of bitcoin, Ethereum, and Solana in 2026, supported by Zerohash infrastructure.

This remains highly regulated, with strict risk scoring and allocation software limits. But it effectively makes crypto a mainstream investment option accessible to 80% of U.S. retirement accounts managed by Morgan Stanley.

Why Now? The Policy Window Has Just Opened

Three regulatory changes set the stage for Morgan Stanley’s move.

First, an executive order signed by President Trump in August directed the Department of Labor (DOL) and the Securities and Exchange Commission (SEC) to revisit rules for alternative investments in 401(k)s and IRAs. This order effectively rewrote the boundaries of retirement investing, signaling to financial institutions that regulatory backlash was no longer an issue.

Second, the GENIUS Act, signed in July, established the first comprehensive stablecoin regulation in the U.S. By requiring 1:1 dollar reserve backing and quarterly audits, the law reduced systemic vulnerabilities and convinced institutions that crypto infrastructure now has regulatory legitimacy.

Third, the Department of Labor reversed its cautious 2022 stance on crypto in retirement plans. By allowing trustees to evaluate crypto investments under traditional ERISA standards, the DOL normalized the inclusion of crypto in 401(k)s and IRAs without special exemptions.

Together, these changes created a narrow policy window. Morgan Stanley was the first mainstream wealth manager to seize the opportunity, while competitors like Fidelity and Schwab moved more slowly as their internal risk committees continued to debate exposure limits.

After interpreting regulatory signals, Wall Street concluded: the risk of not offering crypto now outweighs the risk of offering it. But there’s a deeper current driving this shift: institutions now call it the “currency debasement trade.”

This aligns with arguments long held by gold enthusiasts and bitcoin supporters. Central banks will not stop printing money. Fiat currencies will lose purchasing power. Traditional safe-haven assets like gold are soaring, the dollar index is in a multi-year downtrend, and investors are turning to fixed-supply assets. What was once a fringe idea is now institutional consensus. Bitcoin is now designed as a debasement-resistant asset: fixed supply, transparent issuance, and trustless verification. When money itself is being repriced, bitcoin no longer looks speculative, but rather like capital preservation.

Next Steps

Morgan Stanley’s decisive move puts pressure on other wealth managers with retirement businesses. Here’s where the major players stand.

Fidelity launched a zero-fee crypto IRA in 2022 and now offers spot bitcoin ETFs. As the largest 401(k) provider, holding over a third of U.S. accounts, Fidelity has expanded to include Ethereum and Solana funds. However, it has yet to integrate crypto into advisor-managed retirement portfolios.

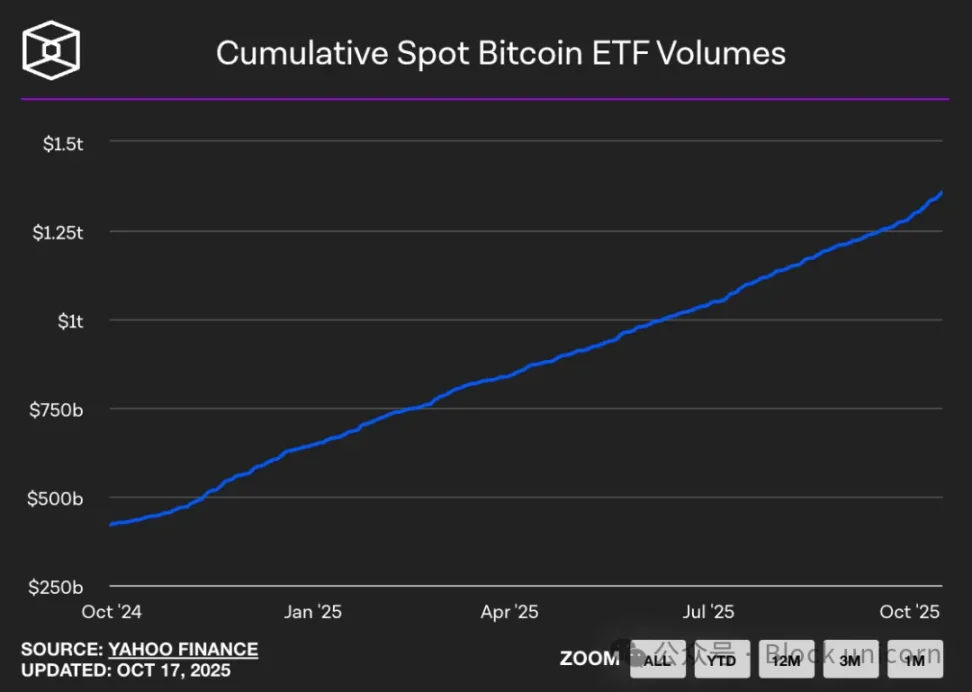

BlackRock’s bitcoin ETF (IBIT) holds $84 billions in assets, commanding 57% of the bitcoin ETF market. It is the fastest-growing ETF in history and may reach $100 billions in 450 days. BlackRock’s strength lies in product dominance, not distribution channels.

Schwab plans to launch spot crypto trading in 2026, targeting Gen Z investors who account for 33% of new accounts and are under 28 years old. Schwab aims to roll out a full suite of products in early 2026 but has not yet opened retirement account access.

Vanguard, managing $10 trillions in assets, after years of resisting crypto assets, is now exploring access to third-party crypto ETFs. Under client pressure and with BlackRock’s new CEO, Vanguard’s policy has shifted to become more open to crypto. However, among major players, Vanguard remains the most cautious.

Goldman Sachs, through its GS DAP platform in partnership with BNY Mellon, focuses on tokenized money market funds, offering on-chain fund record services. The company is building tokenized asset infrastructure rather than pursuing retail crypto exposure.

The broader banking sector is also taking action. JPMorgan is expanding its JPM Coin for cross-border settlements and servicing crypto funds. Citigroup plans to launch digital asset custody services in 2026 and participates in the G7 stablecoin alliance. Bank of America, Deutsche Bank, UBS, and Barclays are all involved in multinational stablecoin research groups.

A noteworthy new player is Erebor Bank, based in Columbus, Ohio, founded by billionaires Palmer Luckey and Joe Lonsdale, both Trump supporters. Erebor received conditional approval from the OCC in October. This tech- and crypto-focused bank aims to serve emerging businesses in fields like AI and digital assets. Its approval signals that regulatory doors are opening to institutions specializing in crypto banking.

Traditional institutions are racing to integrate crypto into existing wealth management infrastructure, while new players are building crypto-native rails from scratch.

While Morgan Stanley’s move brings crypto into individual retirement accounts, state pension funds have quietly been accumulating bitcoin for over a year.

Wisconsin and Michigan have disclosed holdings in BlackRock’s IBIT and ARK bitcoin ETFs, totaling nearly $400 millions.

The risk appetites of ordinary people and Wall Street institutional investors are rapidly converging. Pension funds operate under fiduciary duty, meaning their managers must demonstrate that every allocation is prudent and in beneficiaries’ best interests. If they are willing to invest in bitcoin, it’s because they believe the diversification benefits and asymmetric upside outweigh the volatility risks.

Now, through Morgan Stanley, retirement accounts are joining this trend, highlighting a massive but quiet reallocation of long-term savings toward digital assets. Conservative strategies limit exposure to 5% of the portfolio, while aggressive allocations can reach up to 35%, depending on risk tolerance.

Bitwise analysts estimate that if 1-2% of the $45.8 trillions in retirement assets shift to crypto, that would mean $450 billions to $900 billions in inflows, potentially pushing bitcoin to $200,000. The first wave of funds could arrive this fall, coinciding with a possible Fed rate cut.

But if crypto drops 70%, that would mean $300 billions in retirement losses, potentially impacting consumer spending and eroding trust in retirement advisors.

What happens when everyone else follows suit?

Deutsche Bank analysts predict that by 2030, due to institutional adoption and a weakening dollar, central banks may hold large amounts of bitcoin and gold. Gold has broken above $4,000 per ounce, while bitcoin trades just below its all-time high.

The dollar’s share of global reserves has fallen from 60% in 2000 to 41% in 2025. This decline has driven record inflows into gold and bitcoin ETFs, reaching $5 billions and $4.7 billions, respectively, in June alone.

JPMorgan analysts estimate that by 2027, stablecoin market growth could translate into $1.4 trillions in additional dollar demand, though this depends on overseas investor interest. The interplay between bitcoin’s rise, stablecoin adoption, and dollar hegemony is still unfolding.

However, it is clear that retirement portfolios are being rebuilt via bitcoin ETFs, whether or not regulators, advisors, or retirees fully understand the implications.

If Fidelity, Schwab, and Vanguard follow Morgan Stanley’s lead, the industry will effectively decide that crypto is no longer an alternative asset. It has become a core asset.

Disclaimer: The content of this article solely reflects the author's opinion and does not represent the platform in any capacity. This article is not intended to serve as a reference for making investment decisions.

You may also like

Ethereum Whales Dump Millions in ETH as Retail Investors Fight Back

$1.5B flows into tokenized gold – Are investors abandoning Bitcoin?

Seek Protocol Joins Forces with ICB Network to Enhance Network Scalability, Advance Cross-Chain Benefits to Users